Dealing with debt can feel like going through a maze, especially when you’re bombarded with generic solutions promising quick fixes. According to a CNBC survey, 70% of Americans reported feeling stressed about their finances, underscoring the need for effective strategies. Unfortunately, one-size-fits-all debt solutions often fall short, leaving you frustrated and no closer to financial freedom.

In this detailed guide, you’ll explore why these generic approaches fail, the emotional toll of debt, the power of customized plans, common myths to avoid, essential support systems, and steps to move forward confidently. By understanding these elements, you’ll be equipped to redefine your path to debt relief.

Key Takeaways

Generic Plans Ignore Individual Needs: One-size-fits-all debt solutions often fail because they don’t account for your specific income, debt types, or financial goals.

Emotions Play a Big Role: Debt is emotionally taxing—causing anxiety, shame, and isolation. Effective debt management must address both financial and emotional stressors.

Personalized Plans Lead to Better Outcomes: Customized debt plans adapt to your lifestyle, income fluctuations, and long-term goals, offering a sustainable path to financial freedom.

Myths Can Mislead You: Common beliefs—like “all debt is bad” or “consolidation fixes everything”—can hinder your progress if left unchallenged.

Understanding Debt Solutions and Their Limitations

Debt solutions encompass a range of strategies, from debt consolidation loans to settlement programs, designed to help you manage or eliminate debt. While these options sound promising, their one-size-fits-all nature often overlooks your unique financial situation, leading to limited success.

Generic solutions, such as pre-packaged debt management plans or universal consolidation loans, assume that everyone’s debt arises from similar causes and can be resolved in the same manner. For instance, a debt consolidation loan might lower your interest rate, but it may fail if your income can’t support the monthly payments. Similarly, debt settlement programs promising to slash balances by 50% may not account for the tax implications or credit damage you’ll face.

These approaches often prioritize speed over sustainability, providing temporary relief but ultimately leading to long-term challenges. Factors such as your income, debt types (e.g., credit card versus medical), and life circumstances, including a recent job loss, require a tailored approach.

Recognizing these limitations sets the stage for a holistic approach to addressing debt. Beyond the numbers, debt carries an emotional weight that generic plans rarely consider, which we’ll explore next.

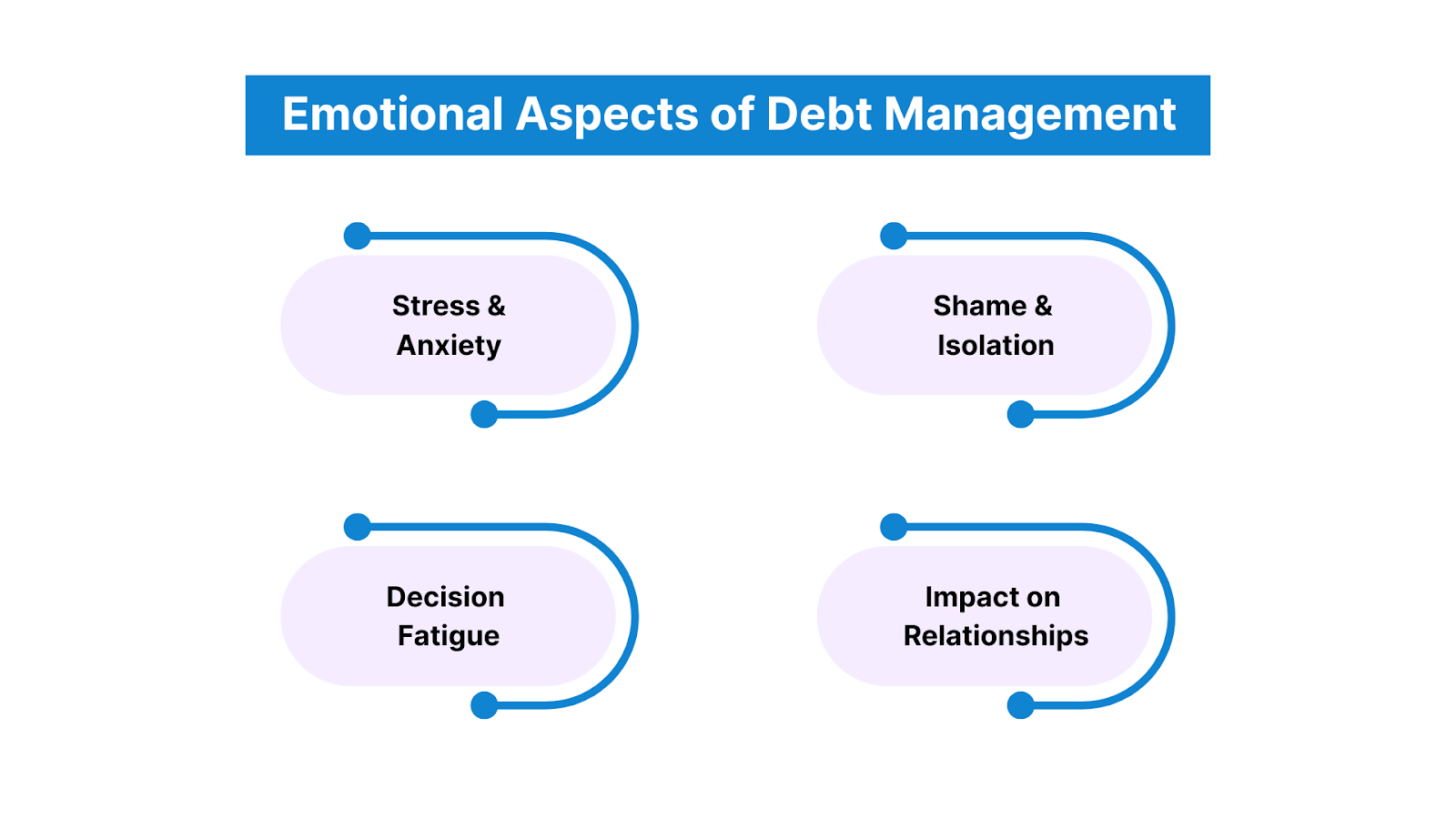

Debt isn’t just a financial burden; it profoundly impacts your emotional well-being. The stress of owing money can affect your mental health, relationships, and daily life, making generic solutions even less effective.

Stress and Anxiety: Constant worry about bills or collection calls can lead to sleepless nights and reduced productivity. Inflation and debt are among the major concerns for most Americans.

Shame and Isolation: You may feel embarrassed about your debt and avoid discussing it with family or friends. This isolation can deepen your sense of hopelessness, making it more difficult to adhere to a rigid, impersonal plan.

Decision Fatigue: Juggling multiple debts and receiving generic advice can overwhelm your ability to make clear choices. For example, choosing between paying a high-interest credit card or a medical bill can paralyze you without personalized guidance.

Impact on Relationships: Financial strain often sparks tension with partners or dependents, especially if a one-size-fits-all plan fails to align with shared goals. Couples may argue over budgeting or sacrifices, eroding trust.

Generic debt solutions rarely address these emotional layers, focusing solely on numbers. A plan that ignores your stress or shame may push you toward unsustainable choices, such as taking on more debt to cover gaps.

Acknowledging the emotional side of debt paves the way for strategies that truly fit your life. Let’s now examine why customized debt plans are essential for lasting success.

The Importance of Customized Debt Plans

A customized debt plan is like a tailored suit; it fits your specific needs, goals, and circumstances, offering a sustainable path to financial freedom. Unlike generic solutions, these plans take into account your unique situation, ensuring better outcomes.

Personalized Financial Assessment: A tailored plan starts by evaluating your income, expenses, debt types, and financial goals. For instance, if you earn $3,000 monthly and owe $20,000 across credit cards and student loans, a plan might prioritize high-interest debt while protecting essential expenses, such as rent.

Flexible Repayment Strategies: Customized plans adjust to your cash flow. If you’re a freelancer with irregular income, your plan might include flexible payments or seasonal adjustments, unlike a rigid consolidation loan with fixed terms.

Goal Alignment: Your plan reflects your priorities, whether it’s rebuilding credit, saving for a home, or avoiding bankruptcy. For example, a debtor seeking to purchase a house might prioritize paying off small debts to quickly improve their credit score.

Emotional Support Integration: Tailored plans often include counseling or support to address stress, helping you stay committed to your goals. A credit counselor can guide you through budgeting and offer tips to manage anxiety about debt.

Adaptability to Life Changes: Life is unpredictable; job losses or medical emergencies can disrupt finances. A customized plan incorporates buffers, such as emergency fund contributions, to mitigate setbacks without derailing progress.

By addressing your specific needs, customized plans increase your chances of success. To fully embrace this approach, you must dispel myths that encourage generic fixes, which we’ll tackle next.

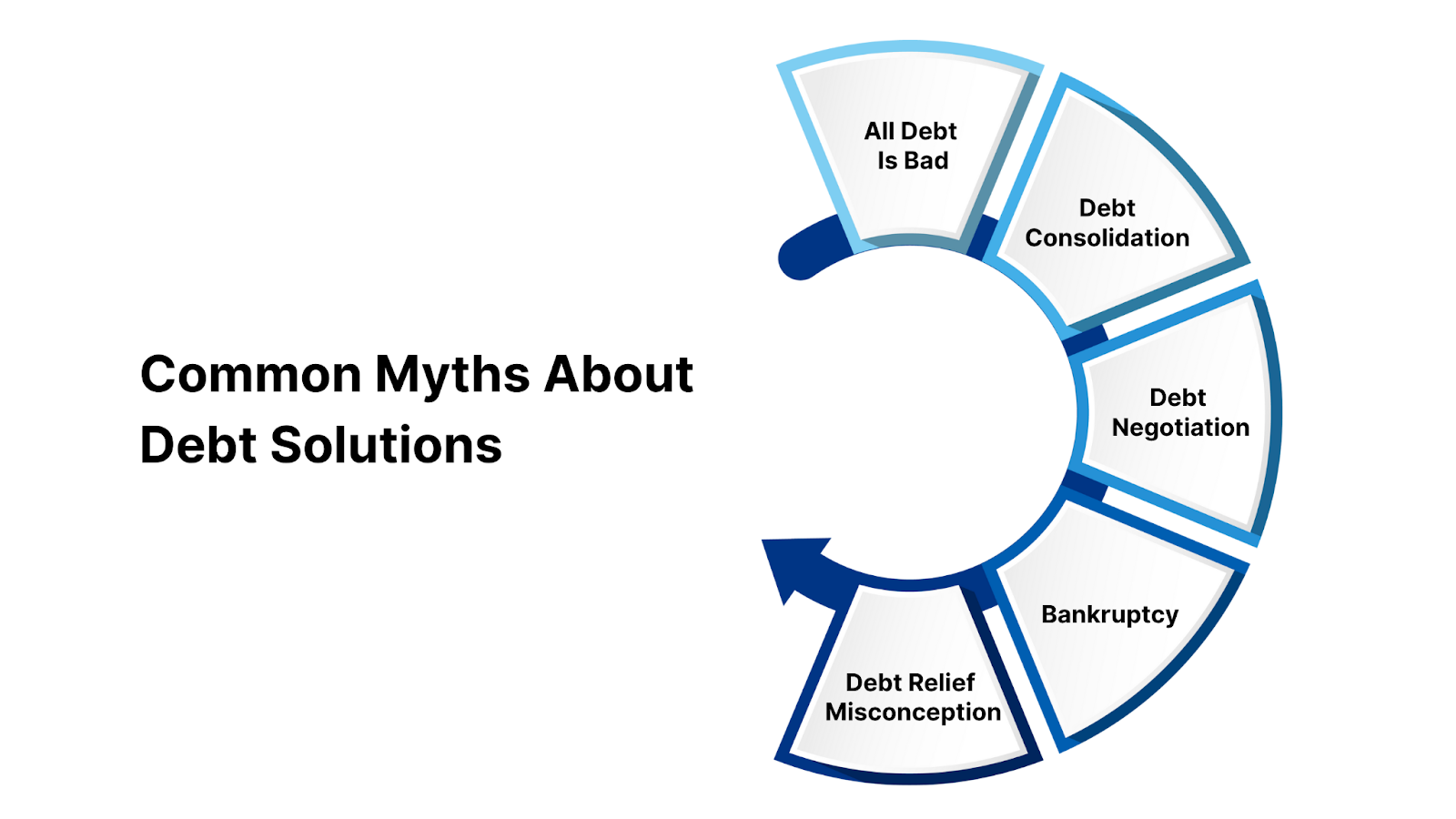

Common Myths About Debt Solutions

Misconceptions about debt solutions can trap you in ineffective strategies, reinforcing the appeal of one-size-fits-all approaches. Debunking these myths helps you make informed choices.

Myth: All Debt Is Bad Not all debt is harmful. Mortgages or student loans, when managed well, can build wealth or skills. Generic plans often treat all debt as equal, prompting you to pay off low-interest loans prematurely when focusing on high-interest credit cards would yield greater savings.

Myth: Debt Consolidation Fixes Everything Consolidation can lower interest rates, but it’s not a cure-all. If your spending habits remain unchanged, you may incur new debt on cleared cards. A tailored plan pairs consolidation with budgeting to address root causes.

Myth: You Can’t Negotiate Debt Many believe creditors won’t budge, but settlement or payment plans are often possible. For example, a $5,000 medical bill might settle for $3,000 with a customized negotiation strategy, something generic programs rarely explore.

Myth: Bankruptcy Ruins You Forever Bankruptcy has long-term effects, but it isn’t a life sentence. Chapter 7 can discharge debts in months, and credit rebuilding starts immediately. Generic advice might steer you away from bankruptcy when it’s the best option for your situation.

Myth: Debt Relief Is Quick Generic programs promise fast results, but sustainable debt relief takes time. A tailored plan sets realistic timelines, such as paying off $15,000 in three years, ensuring you stay motivated without unrealistic expectations.

Clearing up these myths empowers you to seek solutions that fit your reality. Beyond strategies, having the right support systems can make all the difference, so let’s look at those next.

Support Systems and Resources

Tackling debt alone can be daunting, but a robust support network can help keep you on track. These resources provide guidance, accountability, and encouragement tailored to your needs.

Credit Counseling Agencies: Nonprofit agencies, like those accredited by the National Foundation for Credit Counseling, offer personalized debt management plans. They negotiate lower rates with creditors and provide budgeting advice. For instance, a counselor might reduce your credit card interest from 18% to 10%, saving you hundreds.

Financial Advisors: A certified financial planner can help integrate debt repayment into your broader financial goals, such as retirement or homeownership. They might suggest reallocating investments to pay off high-interest debt more quickly, aligning with your long-term financial goals.

Support Groups: Peer groups, such as Debtors Anonymous, offer emotional support and practical tips from others in similar situations. Sharing your story with people who understand can reduce shame and boost motivation.

Legal Aid Services: If facing collection lawsuits, legal aid organizations provide free or low-cost advice. They can help you assert rights under laws like the Fair Debt Collection Practices Act, protecting you from unfair practices.

Online Tools and Education: Apps like YNAB (You Need A Budget) or free resources from the CFPB website provide budgeting templates and debt calculators. These tools empower you to track progress and make informed decisions.

Building support systems equips you with the tools and encouragement needed to stay committed. With these resources in place, let’s focus on how to keep moving forward with confidence.

Overcoming debt requires persistence, and staying motivated is key to long-term success. Here are actionable steps to keep you moving toward financial freedom:

Set Small Milestones: Break your debt journey into achievable goals, like paying off a $1,000 credit card. Celebrate each win, perhaps with a low-cost treat like a coffee, to stay motivated.

Track Progress: Use a spreadsheet or app to monitor debt reduction. Seeing your $20,000 balance drop to $15,000 over six months reinforces your efforts and builds momentum.

Adjust as Needed: Life changes, and so should your plan. If a new expense arises, such as car repairs, work with your counselor to adjust payments without derailing your strategy.

Practice Self-Compassion: If you miss a payment, refocus rather than dwell on guilt. A tailored plan accounts for setbacks, helping you recover quickly.

These steps foster resilience and forward motion, turning debt management into a journey of empowerment. Let’s wrap up with how you can start this journey today.

Conclusion

One-size-fits-all debt solutions fall short because they ignore your unique financial and emotional needs. By understanding their limitations, addressing the emotional side of debt, embracing customized plans, debunking myths, and staying motivated, you can chart a path to true financial freedom. Your debt journey deserves a strategy as individual as you are, one that aligns with your goals and circumstances.

If you’re ready to take control, Forest Hill Management is here to craft a personalized debt solution that works for you. Contact us today to begin your journey toward a brighter, debt-free future.

Frequently Asked Questions (FAQs)

Q1. Why don’t one-size-fits-all debt solutions work for most people? They overlook individual financial circumstances like income, expenses, and the emotional burden of debt. What works for one person may worsen another's situation.

Q2. Can emotions really affect how I manage my debt? Absolutely. Stress, shame, and decision fatigue can lead to avoidance or poor financial choices. Personalized plans often include emotional support to help you cope.

Q3. What does a customized debt plan typically include? It usually starts with a financial assessment and includes tailored repayment strategies, goal alignment, flexibility for life changes, and emotional or educational support.

Q4. Is debt consolidation always a good idea? Not necessarily. While it may lower interest rates, it doesn’t address spending habits or the root cause of your debt. A tailored plan ensures consolidation is part of a larger strategy.

Q5. Where can I find help to build a personalized debt plan? You can work with certified credit counselors, nonprofit agencies, financial advisors, or services like Forest Hill Management that specialize in custom debt solutions.

.png)

.png)