.png)

Facing a debt collection lawsuit can feel overwhelming, especially when you’re unsure how to respond or protect your interests. While these situations are common, knowing how to handle them effectively can significantly minimize their impact on your financial life.

In this comprehensive guide, you’ll learn exactly what a debt collection lawsuit entails, how to review the legal documents you receive carefully, the steps you need to take to respond appropriately, your legal rights and protections, available debt-relief options, how to prepare for court, and what to expect during a hearing.

A debt collection lawsuit happens when a creditor or debt collector sues you to recover money they claim you owe. This usually involves personal debts such as credit card balances, medical bills, or auto loans. The creditor’s goal is to obtain a court judgment, which could give them the power to garnish your wages, seize funds from your bank account, or place liens on your property.

Understanding the nature of these lawsuits is your first step toward crafting a strategic response. The process begins when you’re served with legal documents—often a summons and complaint—that notify you of the lawsuit and demand a response or payment. Ignoring these papers is risky because it could lead to a default judgment, where the court rules against you without hearing your side.

Debt collection lawsuits can come directly from original creditors, like your bank, or from third-party collectors who have purchased your debt. Each case is unique, but your ability to respond thoughtfully depends on having a clear grasp of the documents involved. Let’s dive into how you can carefully review those documents.

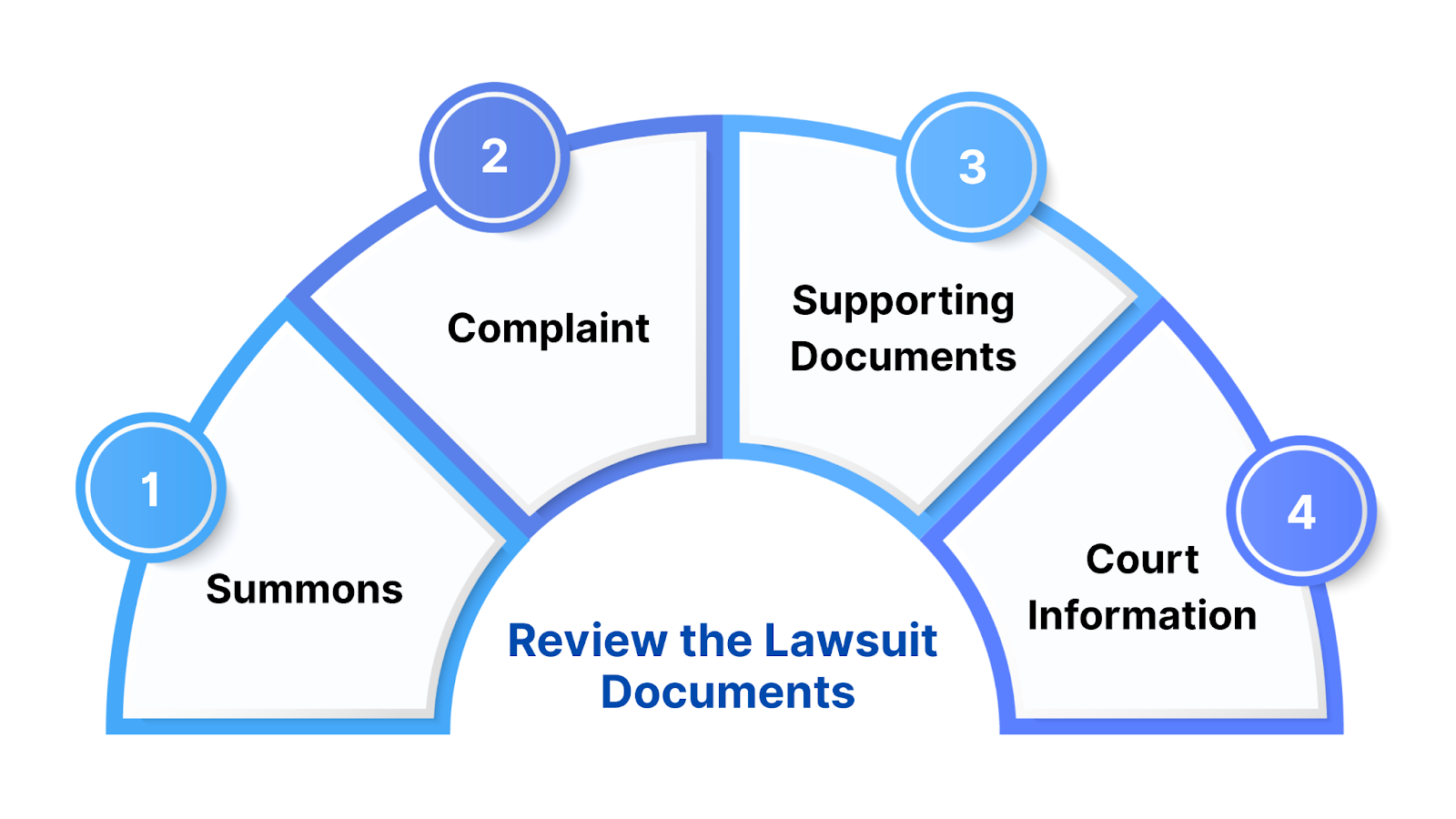

When you receive a debt collection lawsuit, the documents you’re served with contain critical details that will shape your response. Taking the time to examine them thoroughly ensures you understand the claims being made and the deadlines you must meet, setting the stage for an effective defense.

This document informs you that you’re being sued, identifies the court handling the case, and specifies the deadline to respond, typically between 20 and 30 days from the date of service. It’s vital to note the exact date you were served and calculate your response deadline carefully. Missing this deadline can result in a default judgment against you. For example, if you were served on June 1, you might have until June 21 to file your reply.

The complaint outlines the plaintiff’s case, detailing the amount of debt claimed, the creditor’s identity, and the reasons they believe you owe the money. Review this carefully for accuracy. Does the amount match your records? Is the creditor someone you recognize? If you spot errors or inconsistencies, they could provide grounds for challenging the claim.

These might include loan agreements, account statements, or other evidence backing the creditor’s claim. If such documents are missing, incomplete, or don’t support the debt amount claimed, you may have a valid reason to question the debt’s validity. For instance, if a collector claims you owe $5,000, they should provide a contract or payment history to back that up.

Be sure to note the court’s name, location, and case number. This information is essential when filing your response, and if you need to contact the court for procedural questions. Smaller debts are often handled in small claims court, while larger amounts are typically handled in civil courts.

If any part of the documents is unclear or filled with legal jargon, consider consulting a legal professional who can help interpret the details and verify your options. A thorough review of these documents equips you to respond strategically and confidently.

With a solid understanding of the paperwork, you’ll be ready to take the following steps: responding to the lawsuit and protecting your rights.

Also Read: How Credit Card Payment Processing Works: A Simple Guide

Responding to a debt collection lawsuit is crucial to avoid a default judgment, which could result in wage garnishment or asset seizure. Your response, typically referred to as an “answer,” is a formal document filed with the court that addresses the claims in the complaint. Here’s how to proceed:

Responding assertively shows you’re serious about defending yourself. As you prepare your response, knowing your legal rights and protections can strengthen your position, so let’s dive into those next.

You have powerful legal protections when facing a debt collection lawsuit, primarily under the Fair Debt Collection Practices Act (FDCPA) and state laws. Understanding these rights empowers you to challenge unfair practices and build a robust defense.

These protections give you the power to fight back. Beyond defending yourself, exploring debt-relief options can resolve the issue outside court, which we’ll cover next.

A lawsuit doesn’t mean you’re out of options. Debt-relief strategies can settle the matter before trial, saving time and money. Consider these approaches to find a solution that fits your situation:

Exploring these options can lead to a resolution without the need for a trial. If settlement isn’t possible, preparing for court becomes your focus, so let’s look at how to get ready.

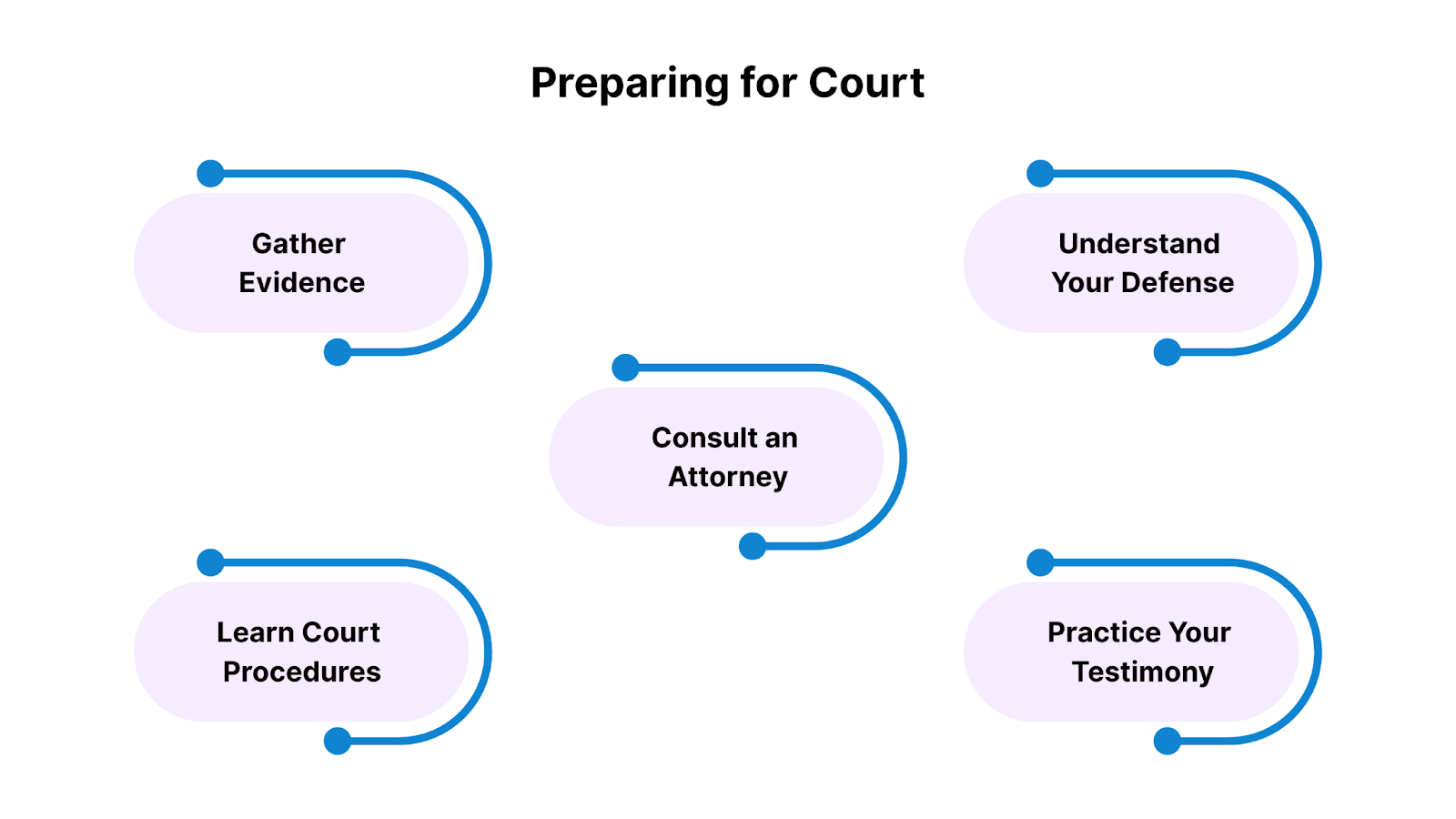

If your case heads to trial, thorough preparation boosts your confidence and strengthens your defense. Here’s how to get ready:

Solid preparation sets you up for success in court. With your case ready, let’s discuss what happens during the hearing.

Also Read: 12 Steps to Reach Financial Independence Early

The court hearing is your opportunity to present your case to a judge, who will decide the outcome based on the evidence and arguments. Knowing what to expect helps you stay composed:

Handling a debt collection lawsuit effectively is a challenging yet achievable goal. By understanding the lawsuit process, carefully reviewing documents, responding promptly, exploring debt-relief options, preparing thoroughly for court, and attending the hearing with confidence, you can protect your interests and regain control of your finances. Each step empowers you to face the challenge head-on, whether you settle out of court or defend yourself in front of a judge.

If you’re feeling uncertain or need expert guidance, Forest Hill Management is here to support you. Our experienced team can provide tailored strategies to manage debt lawsuits and safeguard your financial well-being. Contact us today to take the first step toward a brighter, more secure future.

Q1. What is a debt collection lawsuit, and why am I being sued?

A debt collection lawsuit occurs when a creditor or collector takes legal action to recover unpaid debts. You're likely being sued due to missed payments on loans, credit cards, or medical bills.

Q2. What should I do when I receive a summons and complaint?

Review the documents carefully, verify the debt details, and note your deadline to respond. File a formal answer with the court to avoid a default judgment and preserve your legal rights.

Q3. Can I settle the debt after being sued?

Yes, you can negotiate a settlement even after a lawsuit is filed. Creditors may accept a reduced amount or payment plan to avoid further legal costs. Always get the agreement in writing.

Q4. What legal defenses can I use in a debt collection case?

Common defenses include expired statute of limitations, incorrect debt amount, mistaken identity, or lack of proper documentation. You can also countersue if your rights under the FDCPA were violated.

Q5. What happens during the court hearing?

The judge hears both sides. You’ll present your defense, and the creditor presents their claim. Bring all supporting documents and stay calm. The judge may rule immediately or later in writing.