.png)

Debt collection can feel like a daunting challenge, often creating stress for both creditors seeking payments and debtors managing financial obligations. New technologies are changing this process, introducing tools that make it easier to resolve debts with less friction and greater fairness, offering a modern approach that benefits everyone involved.

In this comprehensive guide, you’ll learn all about how fintech is transforming debt collection, including future trends in this space. By understanding these developments, you’ll see how technology is reshaping debt collection for better outcomes.

Debt collection has historically been a labor-intensive process, relying heavily on phone calls, mailed notices, and in-person negotiations. Collectors often faced resistance, as debtors felt pressured or harassed, leading to strained interactions and low recovery rates. Traditional methods were also time-consuming, with manual record-keeping and limited ability to personalize outreach.

The rise of fintech has reformed this industry. Since the early 2010s, financial technology companies have introduced tools like automated communication platforms, artificial intelligence, and blockchain to streamline operations. These innovations have shifted debt collection from confrontational tactics to more transparent and collaborative approaches.

For example, instead of relentless calls, you might receive a text with a payment link tailored to your financial situation. This evolution has made the process more efficient for creditors and less intimidating for debtors, setting a new standard for the industry.

Fintech’s impact starts with modernizing core processes. To understand how these changes take shape, let’s examine the digitization of debt collection practices.

Also Read: Steps to Create a Successful Business Financial Plan

Digitization has transformed how debt collection operates, replacing outdated methods with automated, technology-driven solutions. This shift saves time, reduces costs, and improves accuracy for both collectors and debtors.

These digital tools make debt collection faster and more transparent. Beyond operational efficiency, fintech enhances how collectors interact with you, which we’ll explore next.

Fintech has shifted debt collection toward a more customer-centric approach, prioritizing empathy and flexibility over confrontation. This change benefits you as a debtor by reducing stress and fostering cooperation.

Modern platforms enable personalized communication that respects your preferences. Instead of generic letters, you might receive a tailored email suggesting a payment plan based on your financial profile. For example, if you’re struggling with a $3,000 medical bill, a fintech tool might offer a 12-month plan with $250 monthly payments, aligning with your budget. These systems often allow you to choose communication channels, like text over calls, making interactions less intrusive.

Fintech also provides self-service options. Online dashboards let you check your balance, explore repayment options, or request a settlement without speaking to a collector. This empowers you to manage your debt on your terms, reducing anxiety. Additionally, AI-driven chatbots offer 24/7 support, answering questions like “Can I extend my payment deadline?” at any time, unlike traditional agencies with limited hours.

By focusing on your experience, fintech creates a more collaborative process. This improved interaction is closely tied to payment convenience, our next topic.

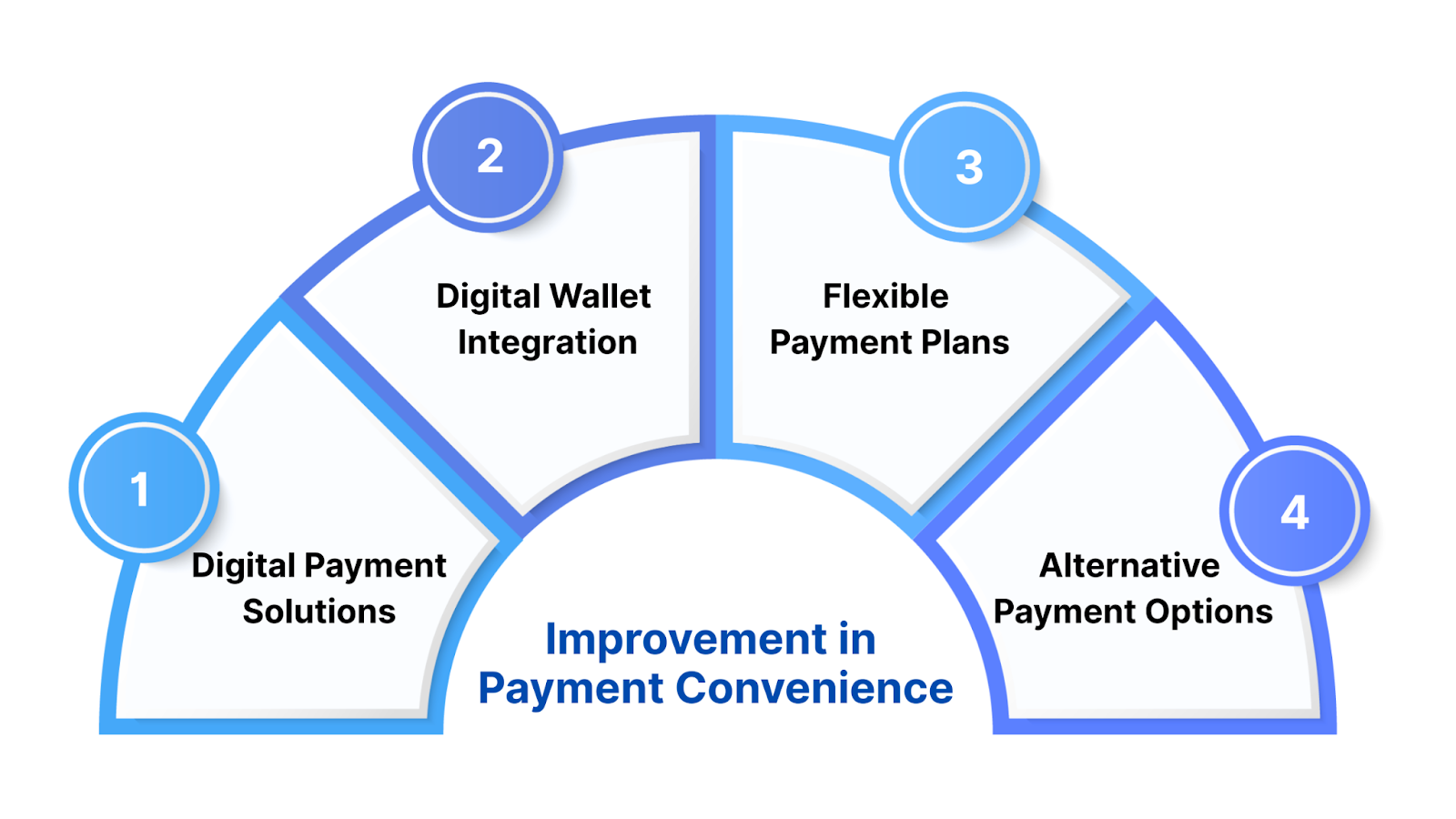

Fintech has made paying debts easier and more accessible, encouraging timely repayments while reducing friction for you. These advancements ensure you can settle debts in ways that suit your lifestyle. Here are some ways fintech has improved convenience:

These convenient payment methods make it easier for you to stay on top of your debts, fostering a sense of control and reducing stress. Enhanced convenience makes repayment more achievable, but compliance with regulations is equally critical, which we’ll cover next.

Debt collection is heavily regulated, with laws like the Fair Debt Collection Practices Act (FDCPA) protecting you from unfair practices. Fintech ensures compliance while streamlining operations, balancing legal obligations with efficiency.

Advanced software tracks regulatory requirements in real-time, ensuring collectors adhere to rules like limiting contact frequency or avoiding harassment. For example, if the FDCPA restricts calls after 8 p.m., a fintech platform can automatically schedule texts within permitted hours, keeping interactions lawful and respectful. This reduces your stress and protects your rights.

Fintech also simplifies compliance documentation. Automated systems generate records of every interaction, such as emails sent or payments received, creating a clear audit trail. If you dispute a $2,500 debt, the collector can provide verified records to resolve the issue, avoiding legal escalation. Some platforms use AI to flag potential violations, like an overly aggressive message, before it reaches you.

For global or multi-state operations, fintech adapts to varying regulations. If you’re in California, where state laws cap collection fees, the platform adjusts terms to comply, ensuring you’re not overcharged. These solutions create a fairer process. With compliance in check, let’s look at how fintech strengthens security and fraud detection.

Also Read: 8 Steps and Strategies for a Debt-Free Plan

Protecting your financial information during debt collection is crucial, and fintech introduces robust tools to enhance security and prevent fraud.

Blockchain technology, used by some fintech platforms, creates secure, tamper-proof records of transactions. If you pay $500 toward a debt, blockchain ensures the payment is logged accurately, reducing disputes over misapplied funds. Encryption safeguards your data, like bank account details, when you use an online payment portal, protecting you from breaches.

AI-driven fraud detection systems analyze patterns to spot suspicious activity. For instance, if a payment is attempted from an unusual location, the system flags it and alerts you, preventing identity theft. Biometric authentication, like fingerprint or facial recognition, adds another layer of security when you access debt collection apps, ensuring only you can manage your account.

These measures build trust in the process. If you’re concerned about sharing sensitive information, fintech’s security features give you peace of mind. Beyond protecting your data, fintech uses data to make smarter decisions, our next focus.

Fintech empowers debt collectors with data analytics, enabling tailored strategies that benefit both you and the creditor. By analyzing your financial behavior, these tools create more effective repayment plans.

AI algorithms assess your payment history, income, and spending patterns to suggest realistic payment options. For example, if you’ve struggled with a $6,000 debt but consistently pay $200 monthly on other bills, the system might propose a similar plan, increasing the likelihood of success. This data-driven approach avoids unrealistic demands, like a $2,000 lump sum, that could push you into further financial strain.

Predictive analytics help collectors prioritize accounts. If data shows you’re likely to pay with gentle reminders, they might focus on automated texts rather than calls, saving time and reducing pressure. For creditors, analytics improve recovery rates by identifying which debtors are most likely to repay, allowing them to allocate resources efficiently.

Data also benefits you by personalizing solutions. If you’re a freelancer with irregular income, analytics might suggest flexible payment schedules, like higher payments in high-earning months. This tailored approach enhances outcomes. As fintech continues to evolve, let’s explore what’s next for debt collection.

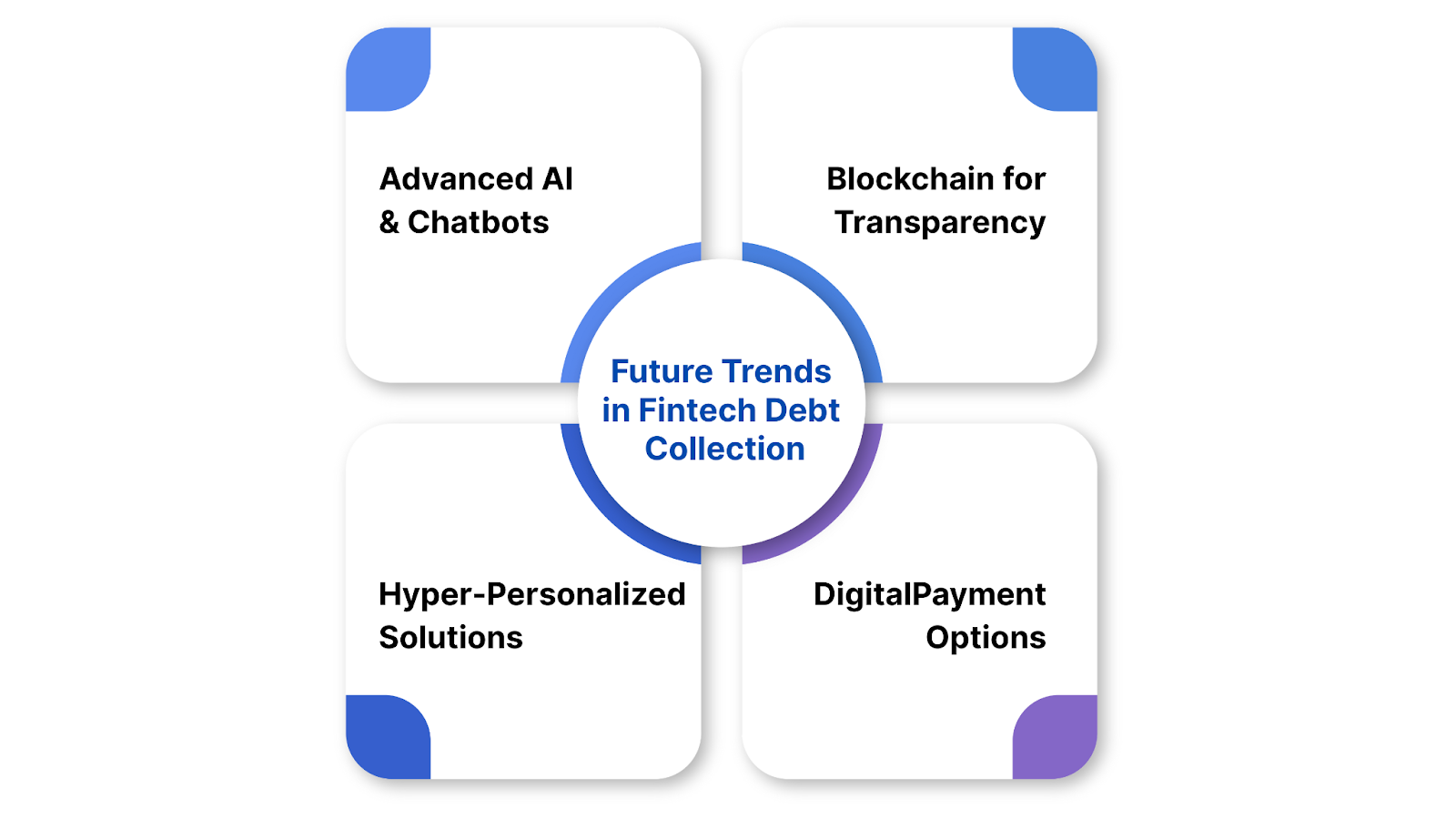

The debt collection industry is on the cusp of further innovation, with fintech driving advancements that will make the process even more efficient, transparent, and user-focused. These emerging trends are set to reshape how you interact with creditors, offering smarter tools and more personalized solutions. Staying informed about these developments prepares you for a future where debt collection is less intimidating and more collaborative.

These trends point to a future where debt collection is more seamless and fair, empowering you with greater control.

Modern technology has transformed debt collection into a more efficient and equitable process. From digitized operations and enhanced customer experiences to convenient payments, compliant practices, secure systems, data-driven strategies, and exciting future trends, fintech is reshaping debt collection for the better.

Forest Hill Management uses these technological advancements to support your needs. Our team designs personalized debt collection strategies for creditors and debtors. We simplify the process while prioritizing fairness and efficiency. You can achieve better financial outcomes with our expert guidance. Contact our team today to start a smoother debt collection journey.

Q1. How do fintech tools make debt collection easier for me as a debtor?

Fintech platforms offer user-friendly options like online portals and mobile apps, allowing you to view your debt, negotiate terms, or make payments anytime. These tools also provide personalized communication, like texts instead of calls, reducing stress. Forest Hill Management uses these technologies to create tailored solutions, helping you manage debts with ease.

Q2. Are fintech debt collection platforms safe to use?

Yes, fintech platforms prioritize security with tools like encryption and blockchain to protect your data. AI-driven fraud detection flags suspicious activity, like unauthorized payments. Forest Hill Management partners with secure fintech solutions to safeguard your information, giving you peace of mind during debt collection.

Q3. How does fintech ensure debt collectors follow regulations?

Fintech software tracks laws like the Fair Debt Collection Practices Act, scheduling contacts within legal hours, such as texts before 8 p.m. Automated systems document every interaction, creating a clear audit trail if you dispute a debt.

Q4. Can I customize my debt repayment plan with fintech?

Absolutely. Fintech platforms analyze your income and spending to propose affordable plans, like $150 monthly payments for a $2,500 debt. You can often adjust payment dates to align with your paycheck.