.png)

In 2023, the CFPB received approximately 109,900 complaints related to debt collection practices, with nearly half involving attempts to collect debts not owed. That number paints a vivid picture of how common it is for consumers like you to encounter aggressive or unfair tactics when dealing with debt collectors.

Thankfully, the Fair Debt Collection Practices Act (FDCPA) steps in to shield you from such experiences. In this detailed guide, you’ll discover what the FDCPA entails, who it regulates, its essential rules, the practices it forbids, limits on collector communication, how it’s enforced, and how state laws might enhance your protections. Armed with this knowledge, you can tackle debt collection confidently and protect your rights.

The Fair Debt Collection Practices Act, often referred to as the FDCPA, is a federal law introduced in 1977 to safeguard consumers from abusive debt collection practices. Its core mission is to ensure that you’re treated fairly and respectfully when someone attempts to recover a debt you owe. This law applies to personal debts like credit card balances, medical bills, or car loans, but it doesn’t cover business-related debts.

The FDCPA emerged from a need to curb widespread misconduct by debt collectors, balancing their right to pursue owed funds with your right to dignity and privacy. It’s a cornerstone of consumer protection, giving you tools to challenge unfair treatment. With this background in mind, let’s clarify who exactly qualifies as a debt collector under this law.

Also Read: 8 Ways to Develop Good Financial Habits

Under the FDCPA, a debt collector is generally a third party tasked with collecting a debt on behalf of someone else. This category includes collection agencies, companies that buy delinquent debts, and even lawyers who regularly handle debt collection. However, original creditors, those who first lent you the money, typically don’t fall under this definition unless they disguise themselves as third parties or use a different name to collect.

For instance, if your bank tries to recover a loan directly, they’re not bound by the FDCPA. But if they pass that debt to a collection agency or sell it to another entity, those parties must follow the law. Now that you understand who the FDCPA targets, let’s dive into the key rules these collectors must obey.

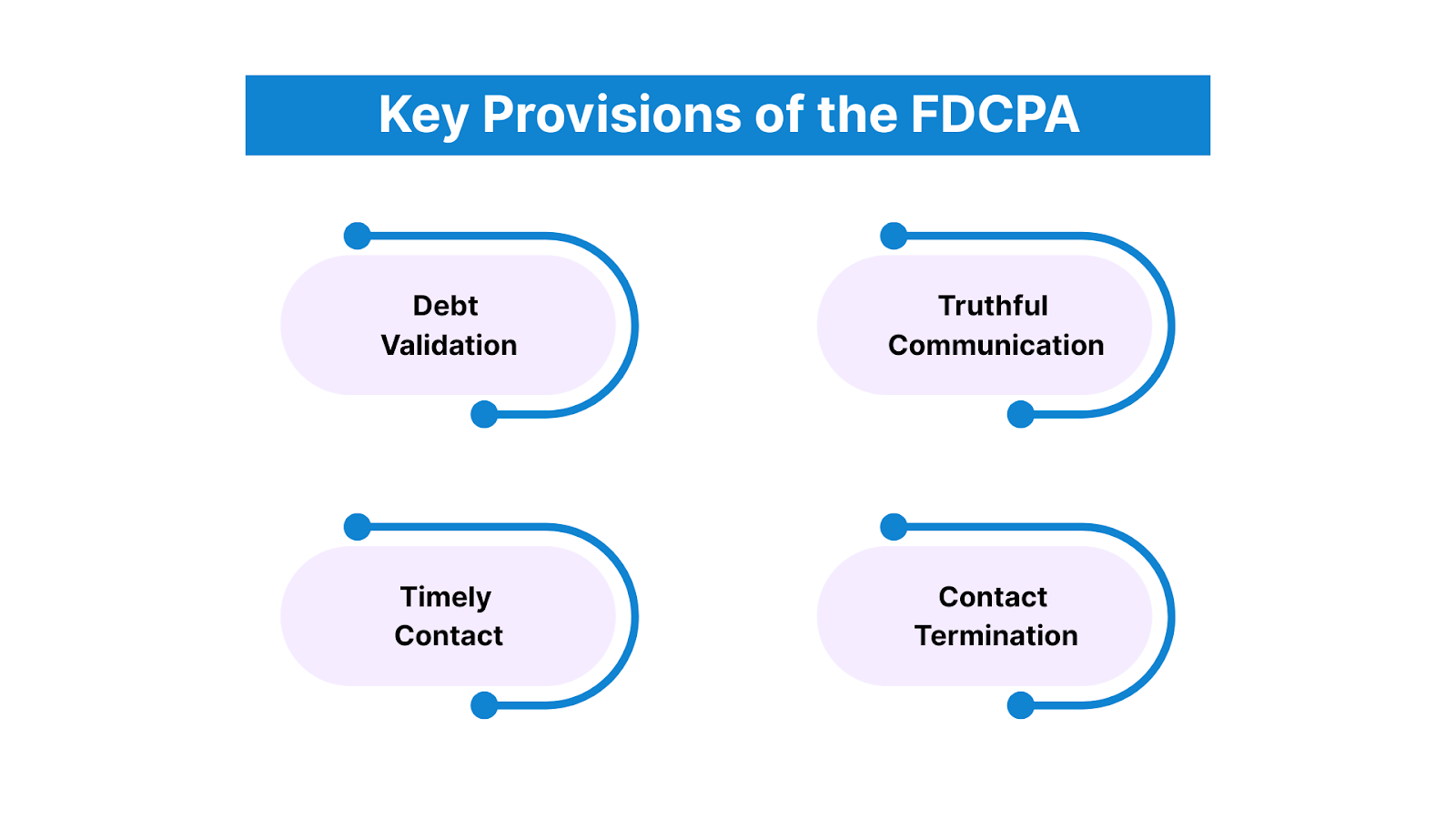

The FDCPA lays out specific guidelines to protect you from overreach by debt collectors. Here are some of its most important provisions:

These rules create a framework for fair debt collection. To build on this, let’s explore the specific actions debt collectors are prohibited from taking.

The FDCPA doesn’t just set rules; it also explicitly bans certain behaviors to shield you from harassment or deceit:

These prohibitions keep debt collection within ethical bounds. Next, let’s look at how the FDCPA restricts when and how collectors can contact you.

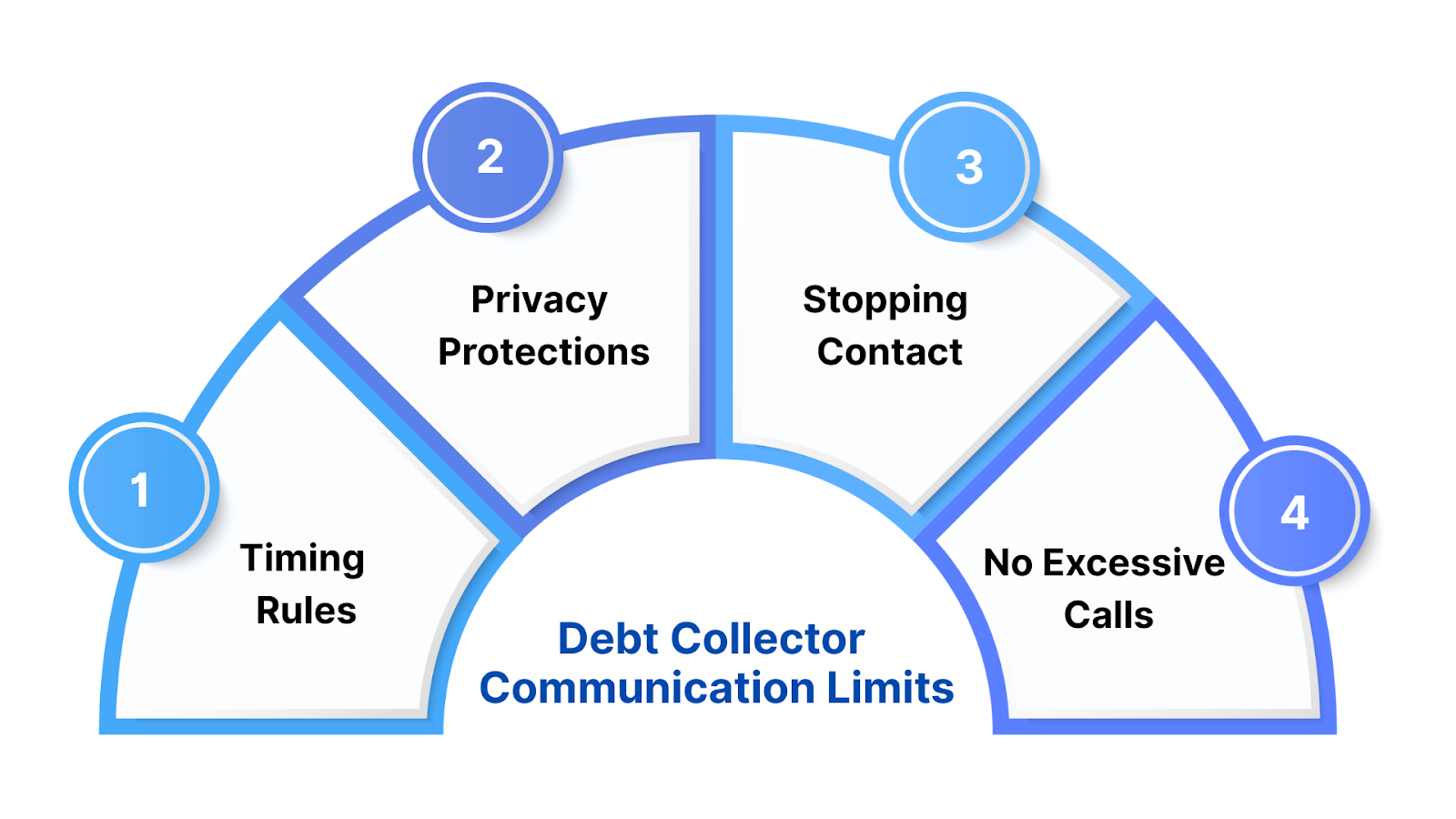

To prevent debt collectors from overwhelming you, the FDCPA imposes strict communication limits:

These boundaries help maintain your peace of mind during debt collection. With these limits established, let’s examine how the FDCPA is enforced when violations occur.

When debt collectors break the rules, the FDCPA provides several ways to hold them accountable:

To enforce your rights, keep records of all collector interactions, phone logs, letters, or voicemails, and file complaints with the CFPB or FTC if needed. Knowing how the law is upheld is empowering, but you might also benefit from state-specific rules, which we’ll cover next.

Also Read: 7 Personal Finance Tips for Better Money Management

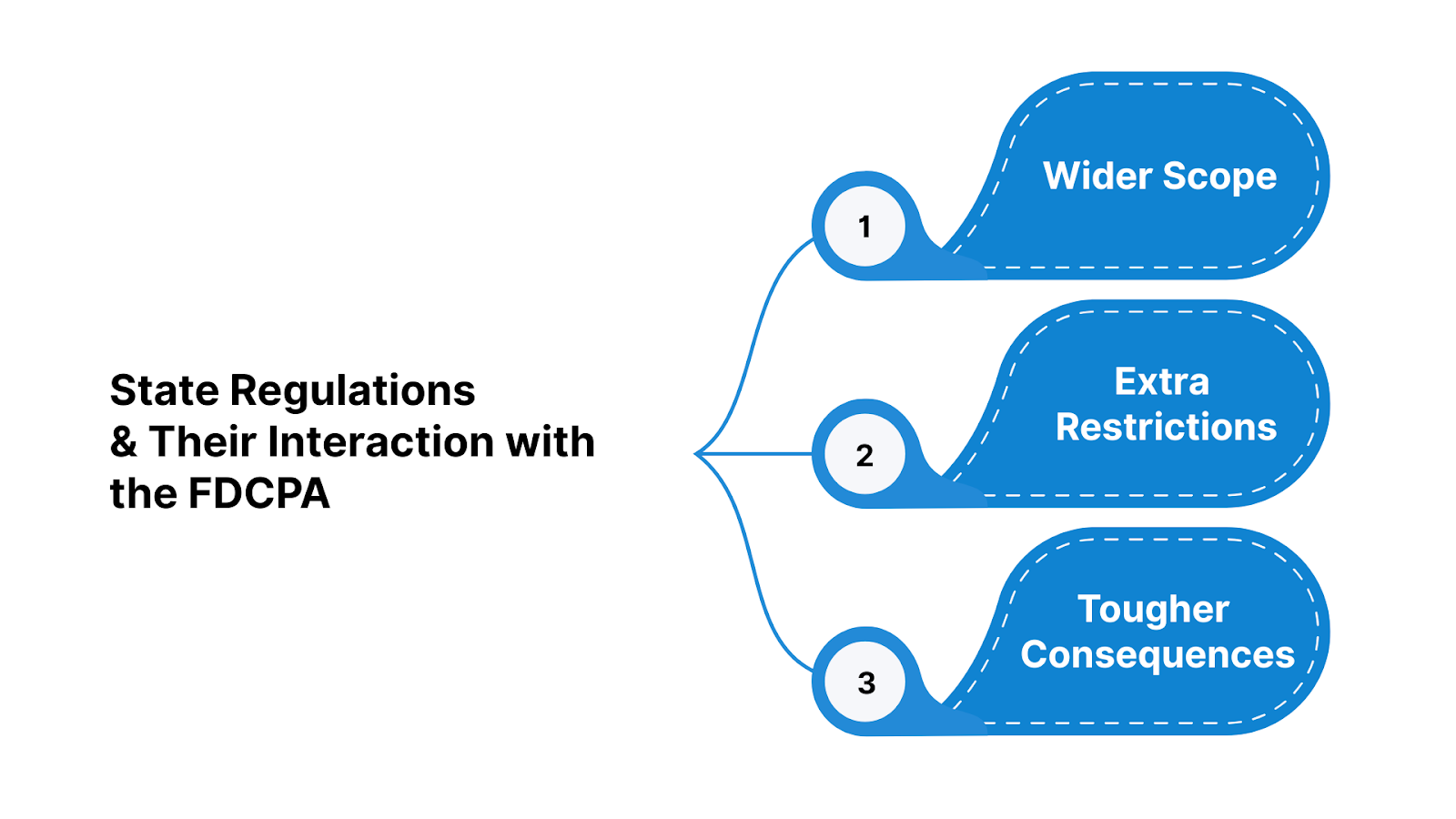

The FDCPA sets a federal baseline, but many states enhance these protections with their own laws:

When federal and state laws differ, you get the benefit of the stricter one. Checking your state’s regulations alongside the FDCPA ensures you’re fully informed. With this dual-layer protection in view, let’s wrap up with some final thoughts.

The Fair Debt Collection Practices Act stands as your shield against unfair debt collection practices. By grasping its scope, who it governs, core rules, banned actions, communication limits, enforcement options, and how state laws complement it, you’re equipped to handle debt collectors confidently.

Forest Hill Management is ready to assist if debt collection feels overwhelming or you’re unsure how to proceed. Our experienced team can offer tailored advice and practical solutions to manage your debt effectively. Reach out today to protect your financial future and gain the support you need.

Q1. What is the Fair Practices Act in the context of debt collection?

The Fair Debt Collection Practices Act (FDCPA) is a federal law that protects consumers from unfair, deceptive, or abusive practices by third-party debt collectors.

Q2. Who is considered a debt collector under the FDCPA?

A debt collector is typically a third party, such as a collection agency, debt buyer, or attorney collecting on behalf of others. Original creditors are generally not covered unless they use deceptive tactics.

Q3. What are my rights under the FDCPA?

You have the right to receive written notice of the debt, dispute it within 30 days, request no further contact, and be free from harassment or misleading threats.

Q4. Can I stop a debt collector from contacting me?

Yes. You can send a written request for them to stop communication. After that, they can only contact you to confirm they’re ceasing contact or to notify you of legal action.

Q5. What happens if a debt collector violates the FDCPA?

You can file a complaint with the CFPB or FTC and may sue the collector within one year. If successful, you could receive up to $1,000 in damages plus attorney fees.